In a free enterprise economy, the price of a good or a service is determined by market demand and market supply. Demand comes from buyers while supply comes from sellers. Market price gets determined as a result of the free interaction between buyers and sellers.

Definition of Demand

Human wants or desires are unlimited but demand is not unlimited. Demand means both the desire to have a good and the ability to pay for that good. Individual desires alone have no effect on decisions made by producers unless they get translated into actual spending on goods. Consumer demand must have an effect on the production process. In economics, demand refers to effective demand i.e. a consumer's desire to have a thing must be backed by his ability to pay for that thing.

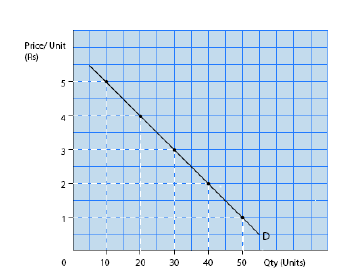

Generally, the quantity demanded of a good tends to increase when its price falls and decrease when its price rises.

The market demand curve is a summation of all the quantities of a good that consumers would buy at a

particular price and at a particular time.

Determinants of Demand :

Its own price - The first factor that determines the demand for a good is the price of that good. When the

price of a good falls, there tends to be an increase in the quantity demanded; and when price rises, there tends to be a decrease in quantity demanded, with the other factors affecting demand remaining unchanged.

Giffen goods -This determines the ability and inability to buy luxury goods.

Expectation of a future price increase - People might purchase more of a commodity at a higher price if they believe that the price will rise further in the near future (e.g. pre- budget purchases of electrical and electronic items or expected changes in share prices).

Ostentatious goods - Demand for articles of ostentation or display will be higher at a higher price than at a lower price (e.g. diamond jewellery, luxury cars, collector's items such as antiques and vintage cars). This would be valid only up to a certain price point and not indefinitely.

Obsolete goods - These are goods which have gone out of fashion such as clothing items that are no longer fashionable. A reduction in the price of an obsolete good is not likely to attract a higher demand.

So far it has been assumed that the demand for a good is determined solely by its own price. But there are many factors other than the price of the good, which affect demand. If any factor other than its own price is considered, a new demand curve has to be drawn. The distinction between a change in quantity demanded and a change in demand is essential to an understanding of how the price mechanism works. A great deal of

confusion can arise if this point is not properly grasped. The former is a movement along a demand curve, while the latter leads to a shift of the entire demand curve. The normal demand curve shows that different quantities are demanded at different price levels, but a shift of the demand curve shows that a different quantity is demanded at each of the original prices.

Changes in Demand

The factors leading to changes in demand and a shift of the entire demand curve are;

- Prices of substitute goods - Substitutes are goods that satisfy the same want. They are competitive products or alternatives to each other.If the price of coffee rises, there tends to be an increase in the demandfor tea with price of tea remaining constant,a fall in the price of coffee tends to lead to a decrease in the demand for tea, with the price of tea remaining the same.

- Prices of complementary goods - These are jointly demanded or inter-related goods so that one is useless without the other.An increase in the price of fuel leads to a decrease in the demand for cars.

- Income - An increase in consumer's money income leads to an increase in demand, with prices of other goods remaining constant. Also, a re-distribution of income in favour of the poorer sections of society will lead to an increase in demand for those goods mostly bought by the poor.

- Tastes and preferences - Over time, new products enter the market and become fashionable (e.g. a particular type of school bag or sports shoes); similarly, some other products might go out of fashion.

- Advertising - An increase in advertising expenditure tends to increase consumer demand (sales).

- Weather and seasonal changes

- Availability of credit facilities

Hi

ReplyDeleteGood post and Nicely explained.you can also visit

http://www.ascentaz.com/services.php

A business and strategy consulting firm in India.Providing result oriented solutions to international and domestic clients.